|

| All images snipped from the Wilshire Report referenced below. |

|

| Over the last ten years the percentage in "equities" has been constant but the mix shifted. US equities decreased by 17% while Non-US equities grew by 7%, Private equity grew by 7% and Real Estate holdings grew by the balance. |

Looking at two pensions that have been in the news:

CalPers has approximately $300B in assets and is funded at 77% of obligations. About 63% of that is in equities and another 10% is in real estate.

Illinois State Pension is $138B in assets and is funded at about 43% of obligations. The Illinois system is strange...it is a bit like the segments of an orange. Rather than do a bunch of non-value added math to add them together I will just report on one of them, the Teachers Pensions. They have about 52% of their assets invested in equities and 13% invested in real estate.

What next?

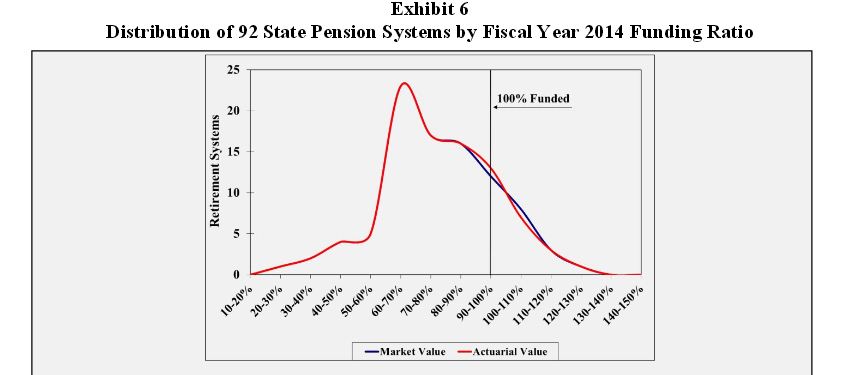

The mode for the Percent Funded is the 60%-to-70% funded bucket. Fully one quarter of all funds examined fell into this bucket.

|

| Regression of Funding Ratio and Equity Allocation |

The rules of estimating funding and future return are a bit arcane. They are allowed to average many year's performance to smooth things out. But in my simple, back-of-envelop way of thinking, 70% exposure * 70% funding means that a 10% drop in the S&P500 (a broad based index of equities) means that their funding ratio dropped about five percent.

That may be one of the biggest reasons the Fed has been juicing up the economy in general and the Stock Markets in general. It was seen as the only way to avoid Pension Armageddon.

It does not look like they will be successful.

I can't help but wonder what is going to happen when the inevitable pension fund crashes occur... Friend of mine's sister took stock in the company rather than diversify, it folded two months after she retired. From $2000/mo to nothing in one fell swoop. She had to go back to work at age 62. She can't live on SSI, knows she will have to sell her house, and severely downsize, but doesn't want to admit it. He's afraid she is going to die at her desk now...

ReplyDeleteI can't help but wonder what is going to happen when the inevitable pension fund crashes occur... Friend of mine's sister took stock in the company rather than diversify, it folded two months after she retired. From $2000/mo to nothing in one fell swoop. She had to go back to work at age 62. She can't live on SSI, knows she will have to sell her house, and severely downsize, but doesn't want to admit it. He's afraid she is going to die at her desk now...

ReplyDelete